Explore how recent Federal Reserve rate changes are influencing mortgage rates today, especially for 30-year loans, and what this means for homebuyers.

Mortgage rates today are under intense scrutiny as recent moves by the Federal Reserve continue to reverberate through the housing market. Homebuyers and homeowners alike are paying close attention, particularly to 30-year fixed-rate loans, which remain the most popular mortgage product in the United States. This week, mortgage rates have shown fresh fluctuations, largely influenced by the Fed’s monetary policy decisions that come amid ongoing efforts to balance inflation control with economic growth.

The surge in mortgage rates earlier this year triggered concerns about affordability and refinancing options, making the latest developments crucial for anyone considering a home loan. Understanding how Fed rate decisions impact mortgage rates today can help prospective buyers and refinancing homeowners make better-informed financial choices.

## Why Are Mortgage Rates Today Trending?

The topic of mortgage rates today has surged in relevance due to the Federal Reserve’s recent adjustments in its benchmark interest rate. Throughout the past month, the Fed has implemented a series of pace changes aiming to curb inflation without halting economic momentum. Investors and economists have been analyzing statements from the Federal Open Market Committee (FOMC) meetings to anticipate how these policy shifts will affect long-term borrowing costs, notably mortgage rates.

Media coverage this week has focused on the Fed’s signals about future rate hikes or pauses, driving mortgage rate expectations and market volatility. This dynamic has led to an increased focus on how such monetary policy will translate into real-world mortgage affordability.

## How Fed Rate Moves Influence Mortgage Rates Today

Though the Federal Reserve sets short-term interest rates, mortgage rates are influenced by a broader range of factors, including bond market trends, inflation expectations, and global economic conditions. Still, the Fed’s rate trajectory directly impacts investor confidence and lender behaviors.

When the Fed raises rates, banks often increase mortgage rates to maintain profit margins and offset higher borrowing costs. Conversely, a pause or rate cut might ease mortgage rates, although the relationship is not always immediate or proportional.

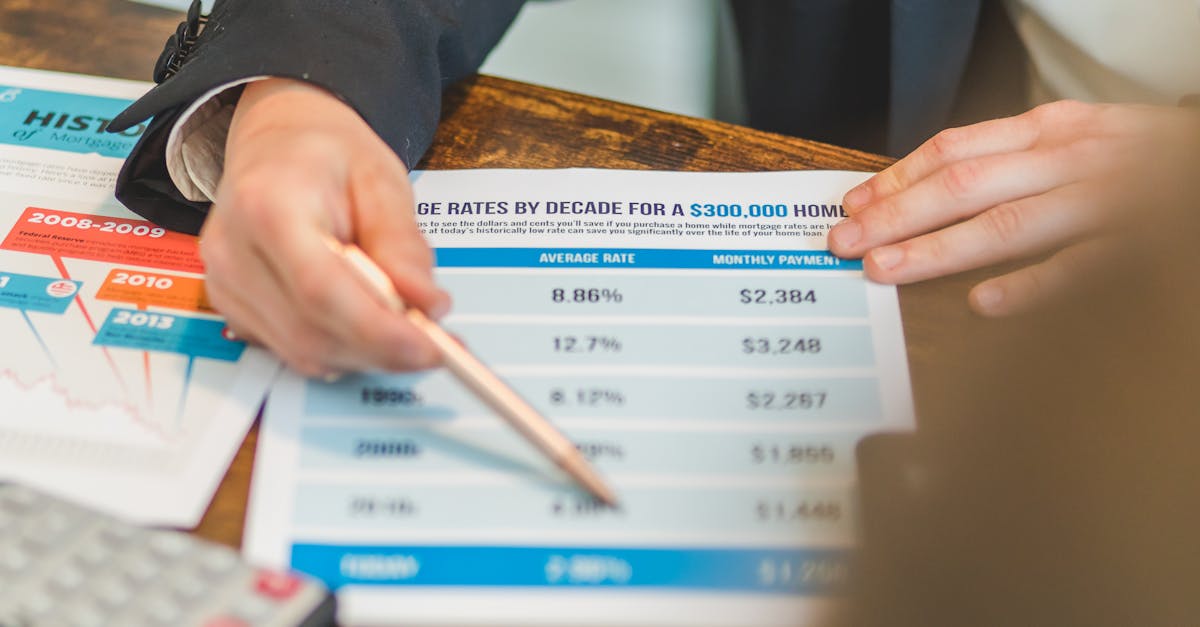

Currently, the Fed’s tightening stance has kept mortgage rates above their historic lows, with the average 30-year fixed mortgage rate hovering around 7% as of early June 2024. While this marks a significant increase compared to the sub-3% rates seen a few years back, it reflects efforts to stabilize inflation and slow housing price accelerations.

## Recent Trends in 30-Year Mortgage Rates

The 30-year fixed mortgage loan remains the gold standard for American homeowners due to its predictable payments and long-term stability. Recent data from Freddie Mac and other mortgage trackers reflect that mortgage rates today for a 30-year fixed loan have fluctuated between 6.8% and 7.2% in the last 30 days, largely tracking the Fed’s policy signals.

Refinancing applications have declined as higher rates reduce the incentive to replace existing loans locked in at lower rates. Meanwhile, purchase mortgage applications have felt the pressure as affordability tightens, although demand remains robust in certain markets with strong employment and housing shortages.

## Expert Insights on Navigating Mortgage Rates Today

Financial advisors and real estate experts recommend prospective homebuyers monitor Fed announcements closely while considering current mortgage rates. Many suggest locking in rates promptly if they are planning large purchases or refinancing because markets can react swiftly to changing economic indicators.

Mortgage professionals also highlight the importance of credit scores and down payment sizes in securing better rates. Even with rates elevated compared to recent memory, individuals with strong financial profiles may still access competitive loan terms.

## Practical Takeaways for Homebuyers and Refinancers

– **Actively Monitor Mortgage Rates Today:** With rates influenced by Fed moves and economic data, staying informed allows timely decisions.

– **Consider Rate Locks:** If you find an attractive mortgage rate, asking your lender about rate locks can protect you from rising costs during the loan processing phase.

– **Improve Your Credit Profile:** A higher credit score can offset the impact of elevated rates by qualifying you for better pricing.

– **Shop Around:** Mortgage rates can vary between lenders; comparing offers helps ensure optimal financing terms.

– **Consult Financial Experts:** Given the complexity of economic factors, professional advice tailored to your situation can help you navigate uncertainties.

## What to Expect Going Forward

As the Federal Reserve continues to balance inflation concerns against economic growth risks, mortgage rates today will likely remain sensitive to any new policy updates or economic releases. Industry watchers expect that if inflation shows signs of cooling consistently, the Fed may slow its rate hikes or pause, potentially stabilizing mortgage rates.

For now, homeowners and homebuyers should plan with the understanding that rates are higher than recent historical lows but reflect a macroeconomic environment aiming for long-term stability in housing and lending markets.

Mortgage rates today serve as a barometer of broader economic conditions, and watching Fed rate moves offers valuable insight into the near-term trajectory of the housing market.

Whether you’re buying your first home or planning to refinance, staying informed about these developments will position you to make smarter financial choices in a shifting interest rate landscape.

**Stay proactive, shop wisely, and consult experts to navigate mortgage rates today confidently.**