Mortgage rates are rising in 2024 due to inflation concerns, affecting affordability for homebuyers. Learn about the reasons behind the increase and how buyers can adapt.

Mortgage rates have risen in 2024, driven primarily by ongoing inflation concerns and shifts in Federal Reserve policies. This increase is impacting homebuyers nationwide by raising borrowing costs and reducing affordability in an already challenging housing market. The topic is trending this week as recent economic reports confirm inflationary pressures have persisted longer than anticipated, prompting lenders to adjust mortgage interest rates upward once again.

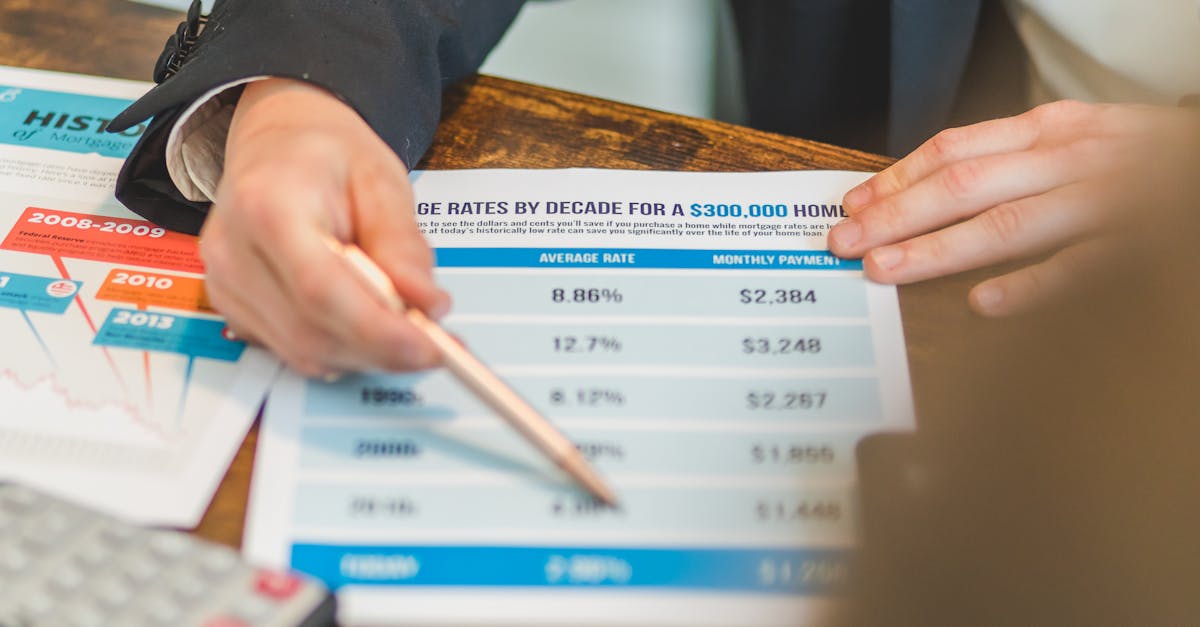

The average rate for a 30-year fixed mortgage has surpassed 7%, levels not widely seen since the early 2000s. This resurgence in rates marks a departure from the historic lows experienced during the pandemic and introduces new financial hurdles for prospective buyers.

## Why Are Mortgage Rates Rising?

The primary driver behind rising mortgage rates is inflation. When inflation accelerates, lenders demand higher interest rates to compensate for the decreased purchasing power of future loan repayments. The Federal Reserve’s monetary policy response to inflation involves increasing benchmark interest rates, which influences mortgage rates directly.

Recent data has shown that inflation remains above the Fed’s target, especially in core components such as housing and services. Consequently, investors require higher yields on mortgage-backed securities, pushing mortgage rates higher.

## Impact on Homebuyers

Higher mortgage rates translate to increased monthly payments. For example, a 1% increase in interest rate on a $300,000 mortgage can raise monthly payments by over $150. This increase can significantly impact home affordability, potentially pricing some buyers out of the market or forcing them to consider less expensive properties.

First-time homebuyers and those with limited budgets are particularly affected. Some may delay purchases or seek alternative financing options as they adapt to rising costs.

## Expert Insights

Mortgage analysts advise that while rates have risen, they remain historically moderate outside the pandemic era. Sarah Thompson, a mortgage expert, explains, “Buyers should stay prepared to act quickly as rates can fluctuate. Locking in rates when possible and improving credit scores can help secure better terms.”

Lenders are also diversifying mortgage products, offering adjustable-rate mortgages and other options to help borrowers manage costs in a rising rate environment.

## How Homebuyers Can Adapt

– **Lock Rates Early:** Secure current mortgage rates when applying to avoid future increases.

– **Maintain Strong Credit:** Higher credit scores can qualify borrowers for better interest rates.

– **Consider Down Payment Size:** Larger down payments reduce loan amounts and monthly payments.

– **Explore Various Loan Types:** Adjustable-rate and government-backed loans may provide better terms.

– **Stay Informed:** Monitor economic trends and consult professionals for tailored advice.

## Market Outlook

Economists expect mortgage rates to remain elevated throughout 2024, barring significant improvements in inflation data. This environment suggests continued pressure on affordability but also potential moderation in housing price growth.

Buyers and sellers should be prepared for a competitive marketplace influenced by these financing challenges.

## Conclusion

Rising mortgage rates amid inflation concerns in 2024 present both challenges and opportunities within the housing market. By understanding the forces at play and adopting strategic financial practices, homebuyers can better navigate the evolving landscape.

Stay proactive, evaluate your options carefully, and seek expert guidance to achieve your homeownership goals in this higher-rate environment.